If your cyber insurance renewal quote arrived recently and the number made you blink twice, you’re not alone. Premiums have climbed sharply, coverage limits have shrunk, and the questionnaires have tripled in length. Underwriters are no longer interested in checkboxes — they want evidence.

And the evidence they want most is something most companies can’t actually produce: a complete, current picture of what they own on the internet.

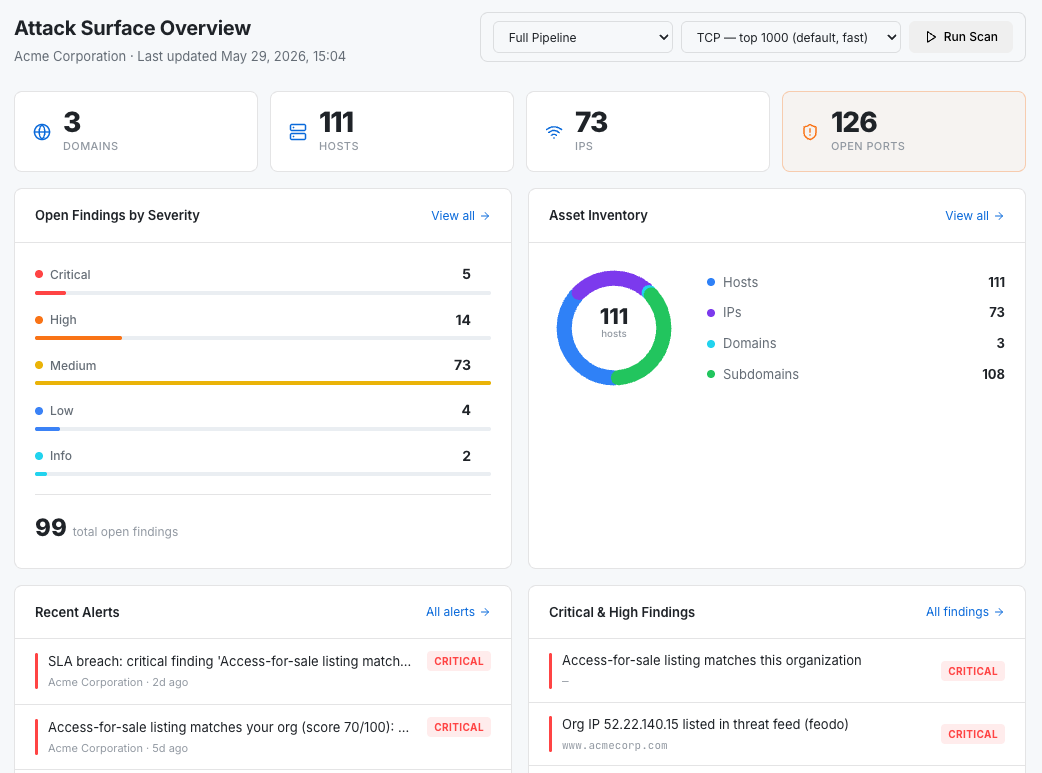

👉 New to ASM and CTI? Start with our plain-English primer: What is ASM? What is CTI? And Why You Need Both →

What Changed in Cyber Insurance

For years, cyber insurance was easy to buy. You filled in a short form, ticked a few boxes about antivirus and backups, and a policy showed up in your inbox a few days later.

That market is gone.

After years of catastrophic ransomware losses, insurers have done the math. They’ve discovered that the businesses filing the biggest claims were often the ones most confidently ticking the boxes. The questionnaires didn’t reflect reality. Companies didn’t know what they didn’t know — and the insurer found out the expensive way.

So underwriters changed their approach. They started:

- Asking dramatically more detailed questions about your internet-facing assets.

- Independently scanning your external footprint before issuing a quote.

- Adding exclusions for incidents traced back to assets you failed to disclose or monitor.

- Raising premiums or refusing renewal when what they see on their scan doesn’t match what you said on your application.

In other words: your attack surface is now a line item on your insurance bill, whether you measure it or not.

The Questions Underwriters Are Actually Asking

Modern cyber insurance applications ask things like:

- Do you maintain a continuously updated inventory of all internet-facing systems?

- Do you scan your external attack surface for vulnerabilities and exposures?

- Are all administrative interfaces (RDP, SSH, admin panels) protected and not exposed to the public internet?

- Do you have MFA on every internet-facing authentication endpoint?

- How quickly do you remediate critical vulnerabilities discovered on external systems?

- Have any of your credentials, domains, or IP ranges appeared in threat intelligence feeds in the last 12 months?

Most companies answer these questions optimistically — because honestly, they don’t know. They’re describing the intended state of their environment, not the actual one.

The problem is that the underwriter often does know. They’re running their own external scans before they price the policy. When their findings don’t match your answers, you don’t get to explain. You get a higher premium, a tighter exclusion clause, or no policy at all.

“Failure to Maintain” — The Exclusion That Catches Everyone

Buried in nearly every modern cyber policy is a clause that goes by names like “failure to maintain controls” or “failure to follow minimum required practices.” The wording varies. The effect is the same: if the breach happened through an asset or weakness you should have known about and failed to address, the insurer can deny the claim.

The harshest part of that clause is the word should. You don’t have to have actually known. You only have to have reasonably been expected to know.

A forgotten subdomain pointing at an expired cloud bucket. A dev environment a contractor spun up two years ago and nobody decommissioned. An admin login page exposed on an old subsidiary domain. None of those things look like risk to the company that owns them — because the company doesn’t remember owning them.

To an insurer evaluating a claim after the breach, every one of those is “should have known.”

Why ASM and CTI Are Now Insurance Tools

Attack Surface Management and Cyber Threat Intelligence — taken together — answer the questions your insurer is now asking, with evidence, on demand.

ASM continuously discovers everything tied to your organization on the internet — domains, subdomains, IPs, cloud assets, exposed services, certificates, login portals. It gives you the inventory the questionnaire assumes you have.

CTI continuously monitors threat intelligence feeds, blacklists, breach dumps, and dark web sources for any sign of your organization being mentioned, targeted, or already compromised — leaked credentials, damaged IP reputation, mentions in attacker forums. It gives you the visibility into “have you been targeted” that underwriters increasingly want to see.

Together, Isaphia ASM + CTI gives you:

- A defensible, current inventory of internet-facing assets — so your questionnaire answers are accurate and provable.

- Early warning on the exposures underwriters scan for — so you can fix them before renewal, not explain them after.

- Documented evidence of continuous monitoring — exactly the kind of operational maturity that lowers premiums.

- A clear paper trail showing what you knew and when — the difference between a covered claim and a denied one.

What You Should Do Before Your Next Renewal

1. Find out what your insurer already sees

Underwriters use the same kind of external scanning that ASM platforms provide. You don’t want the first time you see your external footprint to be on their pricing call. See it first. Fix what you can. Have answers ready for what you can’t.

2. Reconcile your reality with your application

Pull up the cyber insurance questionnaire you filled out last year. Walk through each question. For every “yes,” ask whether you can actually prove it today. The gaps between answered yes and can prove it are your renewal risk.

3. Close the exposures that get scored hardest

Exposed admin interfaces, missing MFA on external logins, expired certificates, known-vulnerable software on internet-facing systems — these are the high-impact findings that move premium math. Most are fixable in days once you know they exist.

4. Make this continuous

A point-in-time audit one month before renewal doesn’t help you. Your attack surface changes weekly. Insurers know that. The companies getting the best terms are the ones who can demonstrate ongoing visibility, not a single annual snapshot.

The Bottom Line

Cyber insurance has stopped being a paperwork exercise and become an operational test. Underwriters are asking you to prove that you know your environment and can defend it — and they have the tools to check.

You can’t insure what you can’t see. And increasingly, you can’t afford not to see it.

How Isaphia Helps

Isaphia ASM + CTI continuously discovers your external attack surface, monitors it against the same threat intelligence and blacklist data your insurer is checking, and gives you the documented, current picture of your environment that today’s underwriters require.

You can see your own attack surface and threat exposure right now, for free. No credit card. No sales call. Sign up and see exactly what your insurer is going to see — before they do.

👉 Start your free trial at app.isaphia.com/signup

Isaphia is an attack surface management and threat intelligence platform that helps organizations discover, monitor, and protect their external digital footprint — before attackers exploit it.